Earnings season is upon us. I love this time of year.

It’s a time for companies to showcase their latest results, including sales and earnings numbers. Investors get to sift through all the updated data… which helps us separate the contenders from the pretenders.

You know me, I’m all about sniffing out the best stocks out there… I love listening to earnings calls. But I understand most folks don’t have the time or patience to sit through all that talking. So let me tell you the one thing to focus on—the most important piece of information you’ll get during an earnings call…

The company’s updated guidance.

Positive guidance means a company is doing better than Wall Street had realized… while negative guidance usually means a company’s outlook is worse than analysts expected.

There are lots of reasons for negative guidance: Sales growth could be slowing… Production might be reduced by supply chain problems… There could be a surprise jump in expenses…

But positive guidance usually has one simple explanation: Business is booming more than anyone expected.

Let’s dig into the details a bit. Then I’ll tell you which sector has the best chance of surprising investors this season.

Guidance is the most important signal

When you think about Wall Street, there’s one important idea to keep in mind…

The future is way more important than the past.

You see, no one really cares about a company’s history. That’s old news. Where it’s headed is more important than where it’s been.

When analysts put a value on a stock, they’re looking at the future numbers.

That’s why guidance is so important. When a company’s guidance is better than analysts were expecting, it means the company’s value could be a lot higher than anyone figured.

On the flip side, when a company issues disappointing guidance, the analysts have to lower their expectations. And the stock price often plunges as investors run for the exits.

Here’s a quick example:

Acme reports earnings and issues guidance for next quarter. The company expects next quarter’s sales to hit $100 million, with earnings of $1 a share. This is above analysts’ expectations for $85 million in sales and earnings of $0.85 a share.

All things being equal, you’d expect the stock price to jump on this news. Why? Because all of Wall Street’s models are based on future sales and earnings of $85 million and $0.85. Now, Acme says those numbers are too low, which means all those models need to be adjusted higher.

Meanwhile, the opposite happens with negative guidance. All of those models now have to be revised down. And the stock is likely to plunge based on this new information.

Think about it. If you’re telling the crowd, “Hey, we’re doing worse than you expected,” how do you imagine they’ll react? That’s right—they’ll sell!

Keep this idea in mind over the next few weeks as you try to separate the winners from the losers. Look for positive upside… prices tend to follow.

So, which sector am I excited for this season?

Semiconductors are primed for acceleration in the coming years

Back in December, I wrote about my investing game plan for 2021. In it, I said I expected two themes to do well this year: ecommerce and semiconductors.

I still like these areas. And since that writing, both ETFs I mentioned in the article are up double digits: The iShares Evolved U.S. Media and Entertainment ETF (IEME) is up 12%… and the VanEck Semiconductor ETF (SMH) is up almost 20% so far in 2021.

I expect semiconductors to steal the show over the next few weeks. Not only have they had incredible performance year-to-date, but something happened last week that gives me added confidence…

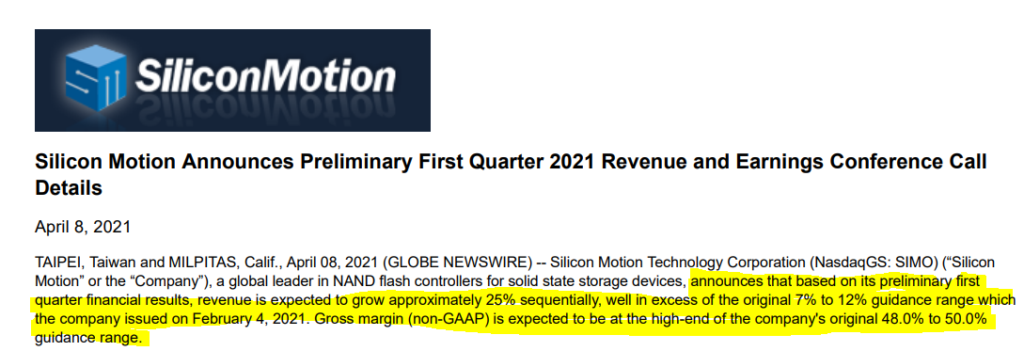

On Thursday, April 8, Silicon Motion Technology (SIMO) issued upbeat revenue and earnings guidance. SIMO is a big player in the NAND flash market. The company’s chips go into storage products like the solid-state drive (SSD) in your computer. Its products also end up in data centers, smartphones, and a variety of commercial and industrial applications.

Not surprisingly, shares of SIMO vaulted to all-time highs on the news.

I added the yellow highlight so you can see what to focus on. Earlier this year, the company said to expect sequential revenue growth in the 7–12% range. In other words, its guidance told investors to expect Q1 sales growth of around 10%.

Now, it’s telling Wall Street to expect 25% growth!

That’s exactly what Wall Street loves to hear. It’s like the foghorn sounding, “All aboard!”

Keep in mind, dozens of semiconductor companies have a similar customer base to SIMO. This leads me to believe other high-quality semi names are likely seeing huge demand. Typically, when one company is doing well, others are too.

For example, Taiwan Semiconductor (TSM) recently announced very strong numbers for March, growing sales 21.2% month-over-month. For a $500B+ company, that’s knockout growth. So, it’s safe to assume semiconductor companies are likely seeing stronger demand across the board.

If you’re looking for exposure to semiconductors, SMH is my favorite way to play the space. This fund owns 25 different names from across the semi industry. If you’re looking for individual stocks I’m zeroing in on—the ones I expect will be tomorrow’s leaders—keep an eye out for Curzio Research’s latest newsletter, The Big Money Report.

The bottom line is this: Guidance is critical to stock prices. Doing a little homework can make all the difference. This is how the pros stay ahead!

Next week, I’ll dig deeper into the latest news from the semiconductor industry. I’ll be looking for more signs of huge upside. I expect to find other firms aggressively raising their numbers, too.